Hydrogen Transformation: Why Does This Market Need Time?

“Project has stalled,” “investments postponed,” “project withdraws from the tender” – these are phrases we increasingly see in today’s hydrogen-sector news stream. For a long time, hydrogen promised to be the solution – a universal energy vector capable of decarbonising sectors that are difficult to electrify. Yet recently many projects have slowed down or even been cancelled. The reasons vary: from costs and financing issues to the lack of real demand from buyers. Before giving in to pessimism, it is worth remembering the “mathematics” of technology deployment. It reveals a simple truth: some technologies simply cannot capture market share quickly – especially when they are being deployed at scale for the first time in history.

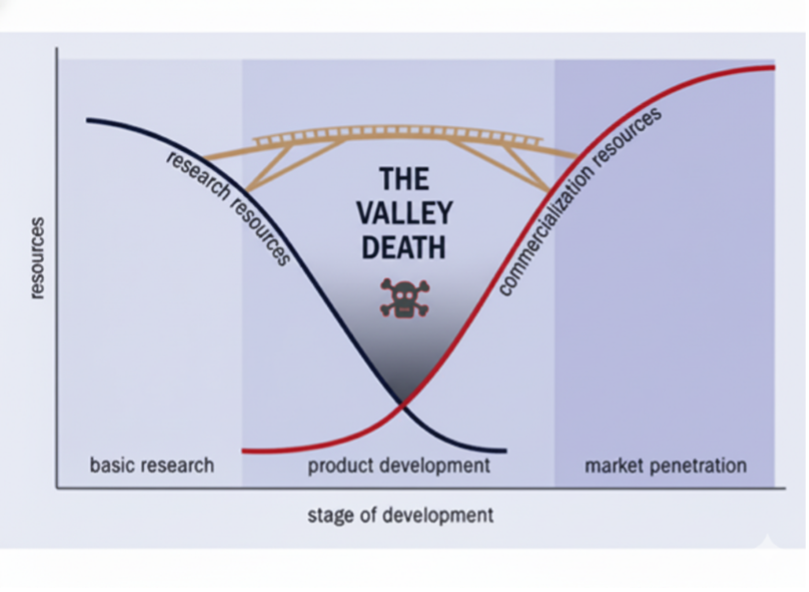

On the Logic of Stages and the “Valley of Death”

The development of new-market technologies occurs in stages: idea → demonstration → scale → market.

Between the demonstration phase and large-scale market commercialization lies the so-called innovation “valley of death” – a gap where the technology is mature enough to attract attention, but still too new or too expensive for private capital to fully commercialize it without additional incentives. This is natural and often means that government intervention becomes essential – through regulation, advance purchase agreements, subsidies, guarantees, or auctions.

A good example is the EV sector: less than a decade ago, electric vehicles seemed like a distant prospect. But after several years of investment, regulation (tax incentives, fuel standards), and market mechanisms, the sector began to grow exponentially. The same is now happening with hydrogen – only here the challenge is not just the technology itself, but also the infrastructure (transportation, storage) and the need for clear, reliable demand from heavy industry consumers.

What Is the European Union Doing About This?

Although hydrogen market development is progressing more slowly, it certainly does not mean the process has stalled. The European Commission is steadily implementing policies to accelerate renewable hydrogen production and develop the necessary storage and transport infrastructure.

These ambitions are reinforced by binding EU targets – for example by 2030, 42% of all hydrogen used in the EU’s industrial sector must come from renewable sources. In the transport sector, hydrogen and its derivatives must account for at least 1% of all energy supplied for transport. Lithuania is also contributing to this direction: according to the national strategy, by 2030 the country aims to install at least 1.3 GW of electrolysis capacity, produce around 129,000 tonnes of green hydrogen per year, and build at least 10 hydrogen refuelling stations.

Because clean hydrogen is still more expensive to produce than fossil-based alternatives, EU funding plays a crucial role in developing the European market. In 2022, the European Commission established the European Hydrogen Bank to finance the entire hydrogen value chain. One of its key instruments today is the EU hydrogen auctions under the Innovation Fund, which support renewable hydrogen production within the EU. The third hydrogen auction is scheduled for December 2025 with an expected budget of €1.1 billion (Across the first three auctions since 2023, the EU has allocated an average of ~€3.7 billion). Plans are also underway to launch import auctions, enabling the purchase of hydrogen from non-EU countries. The European Climate, Infrastructure and Environment Executive Agency are supporting a wide portfolio of hydrogen projects with €5.6 billion in EU funding. Additionally, the new Hydrogen Mechanism – part of the Energy and Raw Materials Platform – has been launched to accelerate the market for renewable and low-carbon hydrogen and its derivatives (ammonia, methanol, eSAF). It will connect supply with demand and link market participants to financing and risk-reduction tools. In Lithuania, political interest is also strong: the Hydrogen Development Guidelines (2024–2050) have been prepared, and a Hydrogen Law is being drafted to provide a legal and strategic framework. In short, Europe is enabling the hydrogen market through regulation, financial instruments, and coordinated market building to ensure a rapid transition to a climate-neutral economy.

Why Hydrogen?

For Europe, hydrogen is more than just another emissions-reduction tool – it is a cornerstone of the entire energy strategy. It helps reduce dependence on imported fossil fuels, strengthening energy security and autonomy. In industry, hydrogen is the only realistic pathway to decarbonize hard-to-electrify sectors – oil refining, steel, cement, and heavy transport. It also enhances grid flexibility by allowing excess renewable electricity to be converted and stored as gas for later use. Ultimately, this entire value chain creates a new economy – from technology and equipment manufacturing to infrastructure and services – reinforcing Europe’s industrial base and leadership in the clean-energy transition.

Conclusion

Hydrogen can be compared to a young, ambitious startup – it has a big vision but still needs financing, partners, and time to establish itself. The technology is still new: after all, we are talking about a fuel produced directly from water rather than fossil resources. This is not an upgrade of existing systems – it is a completely new world, with new mindsets, new transaction models, and entirely new infrastructure.

Our role in this process is to stay calm, maintain consistent regulatory and financial foundations, and trust the direction we are moving in. After all, every successful startup was once just an idea that needed a little time to shine.